Most of us have a natural talent for spending money. In fact, it’s the single easiest thing to do with money! With some taboos around talking about your income, it’s no surprise that spending and specifically our spending habits aren’t things we openly discuss.

So we reached out to our friend Ruth, The Happy Saver, to shine a light on our unanswered spending questions. Ruth helps hundreds of people along their financial journey and you can find more great advice on her blog and podcast.

If you have thought about it, planned for it and saved for it, go ahead and buy it! Then enjoy the item, without regret, once you have.

But if you are shopping on a whim, think you need it, but haven’t planned for it, then you’re better off leaving it in the store, heading home and thinking about it some more. Sleep on it.

Then ask yourself:

You can save for any item, no matter how expensive it is, meaning that when the time is right and the money is there, you can purchase this item and enjoy it.

Leave your wallet at home!

We often impulse buy when out and about doing something else. For example, as you’re walking to a meeting, you might have 10 minutes to spare, and so you pop into the shops. Or before collecting kids from school, it’s easy to stop into the bakery for a snack.

If your wallet is at home it makes these impulse purchases impossible. If you DO still happen to come across something when you are downtown without your wallet, by the time you have made it all the way back home to retrieve your wallet, there is a high chance that you decide it’s not worth the trip back to town to get it!

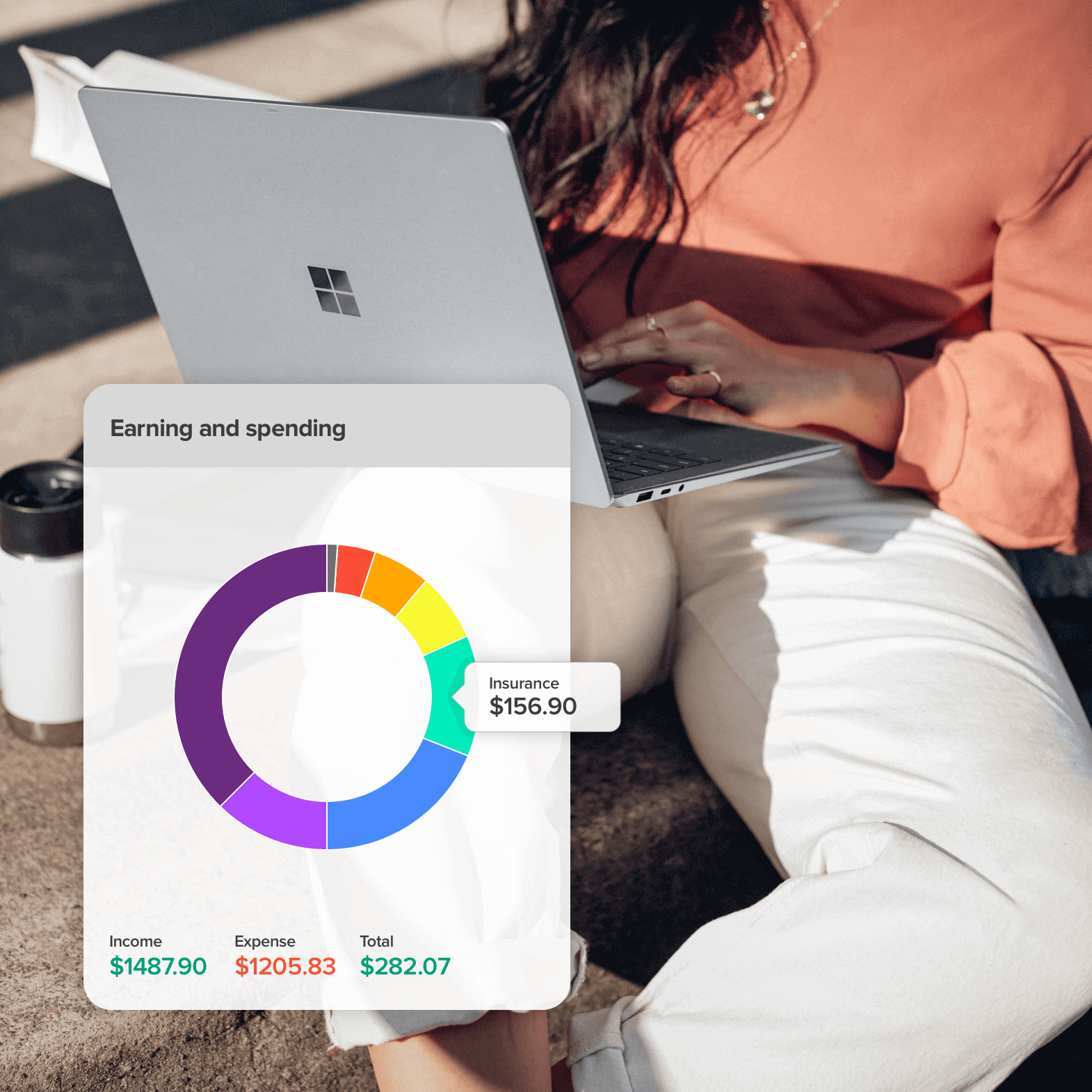

I had to pause and think about this one. So I pulled up my PocketSmith dashboard where I can see a detailed split of categories for my transactions. At a glance a big green one stood out to me - insurance. And watching it grow over as the month ticks along bugs me.

Paying for something that you hope you will never need to use is irritating. However, the rational part of my brain knows that not being covered when an event should occur would bug me even more. And the fact that my entire house was rebuilt by my insurer also reminds me of the importance of having it! So, even though it’s a necessary expense, it still bugs me. Therefore I make sure to do annual check-ups to see that I’m carrying the right amount of insurance for me - not paying too little and not too much either.

The underestimation of the pervasive nature of having debt.

No one wakes up one day to suddenly find themselves $500,000 in debt. Debt is like rust. First, you don’t know it’s there and then it just ever so slowly builds up and grows, sometimes to the point of taking over. Our first debt might be a loan from our parents to buy a car, the second may be a student loan. Both tend to be justified as ‘good’ or ‘safe’ debt because our parents are not out to harm us.

Indeed many think they are teaching a good example of how to handle debt, and the government is offering us money interest-free. Next comes credit card debt or a ‘pay later’ scheme, often followed by a car loan and then the whopper, a mortgage.

It takes a lot to unwind, this bad habit of accepting debt as just being “a part of life”.

One solution is to teach this good money habit from a young age: save up and pay cash for the things you want. Learning to delay gratification will keep you spending mindfully and not reaching for debt to satisfy an immediate need.

That app actually exists within you! It’s called self-control, and everyone has it pre-installed at birth. Some of us may not have updated the app in a while so some features may not be working correctly.

You know that your app needs an update if the following happens:

But it’s a relatively simple fix if you just take the time to install it. You just need to search for the app called “budget” and follow along to get in control of your spending habits again.

We all lead different lives, but for each and every one of us, some things are the same. We sleep, eat, play, create and work. I’m sure there are other things we do, but I’m trying to keep this brief.

Let’s take a look at ‘create’ for a moment. When I think of that word I think of the things we buy or build to create an environment to make us feel enriched, like a painting on the wall, or a beautiful cushion on your sofa. For someone like myself, with few artistic skills, there is no way on earth I could create a painting that I would be able to enjoy looking at on my wall, therefore the convenience of being able to buy a piece of art is always worth the cost. I’m happy to spend my time working to create the income to buy the art.

However, for someone else, the opposite will be true. They may feel their money is better spent buying the canvas, paints and brushes they need and will then spend a lot of their own free time creating the art that they hang on their wall.

So, in answer to that question, I believe it’s a matter not of “how much is my time worth” but instead “what is worth spending my time on” and moving towards doing the things that enrich your life while weighing up convenience and cost along the way. It comes down to what you value in life.

Ruth blogs at thehappysaver.com all about how she and her family handle money. What’s the secret? Spend less than you earn, invest the difference, avoid debt and budget each dollar that flows through your hands. She firmly believes that if you can just get the basics right, life becomes easier from there on in.